Sugar stocks have fallen sharply, with some down as much as 50% from their 52-week highs. This decline is due to several factors, including regulatory actions, rising costs, and market pressures.

First, the government restricted the use of sugarcane for ethanol in the 2023-24 season. This directly impacted the revenue of sugar mills that had invested in ethanol capacities as part of the green fuel push.

Recently, sugarcane’s fair and remunerative price was increased to Rs 355 per quintal for the season starting from October. Although this is good for farmers, it has increased the input costs of sugar mills, putting pressure on their margins.

Meanwhile, the sugar mills have urged the government to raise the sugar’s minimum selling price (MSP) due to increasing operational and procurement costs. However, no revision has been announced so far. Export controls during 2023-24 further impacted the sector.

Read on…

#1 Dwarikesh Sugar

First on the list is Dwarikesh Sugar.

Dwarikesh Sugar operates as an integrated sugar company with a current sugarcane crushing capacity of 21,500 tonnes of cane per day (TCD).

The operations have been integrated into the power and alcohol business, with a 94 megawatt (MW) co-generation capacity and distillery capacity of 337.5 kiloliters per day (KLPD).

The company’s operations are spread across three sugar plants in Uttar Pradesh: Dwarikesh Nagar (DN), Dwarikesh Puram (DP), and Dwarikesh Dham (DD). These plants are strategically located near major sugar-consuming markets in India.

Dwarikesh financial has been affected by regulatory moves. After a strong performance, its financials have shown a downward trend.

Revenue has grown at a compounded annual growth rate (CAGR) of 9.5% to Rs 17 billion (bn) over the last 5 years ending FY24. Net profit declined at a CAGR of 2.6% over the same period.

However, the company’s average return on equity (RoE) and return on capital employed (RoCE) stayed strong at 16%, and 21%, respectively.

Dwarikesh Sugar Financial Snapshot

| Particulars | FY20 | FY21 | FY22 | FY23 | FY24 |

| Sales Growth (%) | 23.2 | 37.6 | 7.6 | 6.3 | -18.7 |

| Net Margin (%) | 5.5 | 5.0 | 7.8 | 5.0 | 4.9 |

| RoE (%) | 15.2 | 15.8 | 23.1 | 14.2 | 10.2 |

| RoCE (%) | 15.5 | 23.1 | 28.6 | 18.7 | 16.9 |

Source: Equitymaster

The company’s financials further deteriorated in 9MFY25. Revenue fell 32% from last year to Rs 9 bn due to lower sugar and ethanol sales volume.

As margins turned negative, the company reported a loss of Rs 0.23 bn, compared to a profit of Rs 0.6 bn.

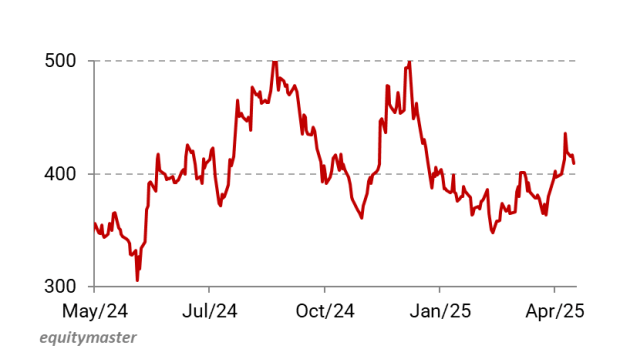

Dwarikesh Sugar Share Price Performance- 1 Year

Looking ahead, the company remains optimistic that it will regain momentum by the 2025-26 season. The announcement of 1 million (m) tons of sugar exports is also a positive development for the sector.

Furthermore, the anticipated increase in ethanol procurement prices and a potential revision in MSP for sugar are expected to boost performance further.

#2 Avadh Sugar and Energy

Next on the list is Avadh Sugar and Energy.

Incorporated in 2015, Avadh Sugar is a part of the K. K. Birla Group.

It manufactures sugar, spirits, ethanol, and other by-products, including molasses, bagasse, press mud, co-generated power, and sanitizers. Sugar contributes 76% of revenue, followed by distilleries (18%) and electricity (6%).

The company operates four sugar mills in Uttar Pradesh with a combined crushing capacity of 39,000 TCD. It also has two distilleries with a total capacity of 325 KLPD, and a co-generation facility with a power generation capacity of 87 MW.

Avadh Sugar’s performance has remained largely stagnant. Revenue has grown at a 4.8% CAGR over the last five years to Rs 26.9 bn, while profits have grown at 1.3% to Rs 1.3 bn.

Export controls, lower ethanol diversion, and rising sugarcane prices weighed on performance. The RoE and RoCE averaged 13% and 20%, respectively, during the period.

Avadh Sugar Financial Snapshot

| Particulars | FY20 | FY21 | FY22 | FY23 | FY24 |

| Sales Growth (%) | 20.2 | 5.9 | 1.2 | 2.0 | -3.7 |

| Net Margin (%) | 3.5 | 2.9 | 4.5 | 3.6 | 4.8 |

| RoE (%) | 15.0 | 11.7 | 15.4 | 11.2 | 12.5 |

| RoCE (%) | 18.9 | 18.7 | 21.1 | 17.8 | 21.6 |

Source: Equitymaster

Growth further weakened in 9MFY25. Total income fell another 5.5% from last year to Rs 19.6 bn due to a 28% drop in ethanol sales volume resulting from policy restrictions.

With lower revenue, the margin contracted to 7%, from a high of 10%. As a result, the company’s net profit crashed 78% to Rs 0.16 bn.

Avadh Sugar Share Price Performance – 1 Year

Looking ahead, profitability will likely recover in FY26, aided by improved sales and the opening of sugar export quotas. Avadh Sugar has received an allocation of 17,377 tonnes from the 1 million tonne export quota.

Additionally, the company plans to invest capital to set up a sugar refinery at Roza and a 100 KLPD greenfield multi-feed distillery.

#3 Dalmia Bharat Sugar

Next on the list is Dalmia Bharat Sugar.

Dalmia Bharat Sugar operates as an integrated sugar company. It is among India’s top five sugar producers with a sugarcane crushing capacity of 44,700 TCD, distillery capacity of 950 KPLD, and co-generation capacity of 138 MW.

The company has the advantage of having capacities in two major sugar-producing states: Uttar Pradesh and Maharashtra.

While the sugar division remains the primary revenue driver, its share has gradually declined to 58% in FY24, from 77% in FY21. In contrast, the contribution of the distillery segment has increased to 38% from 18%.

Dalmia Bharat Sugar Financial Snapshot

| Particulars | FY20 | FY21 | FY22 | FY23 | FY24 |

| Sales Growth (%) | 4.6 | 27.2 | 12.4 | 7.7 | -10.9 |

| Net Margin (%) | 9.2 | 10.1 | 9.9 | 7.6 | 9.4 |

| RoE (%) | 12.7 | 12.6 | 12.6 | 9.2 | 9.3 |

| RoCE (%) | 17.3 | 18.2 | 15.5 | 12.9 | 12.6 |

Source: Equitymaster

Revenue has grown at a stable 8% CAGR over the past five years to Rs 28.9 bn, driven by increasing ethanol and sugar production.

Margin also improved from 15% in FY23 to 19% in FY24. As a result, profit rose 9% to Rs 2.7 bn. Return ratios have been steady, too, with average RoE and RoCE of 11% and 15%, respectively.

Dalmia Bharat Sugar Share Price Performance – 1 Year

Looking ahead, Dalmia Bharat is set to commission an additional 100 KLPD cane-based distillery capacity by April 2025. This facility will start contributing to financials from FY26.

This is part of its plan to transition from a standalone sugar manufacturer to a broader bio-energy player.

The expanded capacity will likely benefit from the government’s continued focus on ethanol blending, targeting 20% blending with automotive fuel by 2026.

#4 Magadh Sugar and Energy

Next on the list is Magadh Sugar and Energy.

Magadh Sugar operates three sugar mills in Bihar, with a crushing capacity of 21,500 TCD.

It also has a total capacity of 155 KLPD and a distillery unit with a co-generation facility with 38 MW power generation. capacity.

Its sugar business contributes 71% of total revenue, followed by the distillery at 23%, and 6% from cogeneration.

Magadh Sugar’s financials have shown steady growth. Revenue grew at 8% CAGR over the past five years to Rs 11 bn in FY24, while profit grew at a 28% CAGR to Rs 1.2 bn. RoE and RoCE also averaged 10% and 18% during the period.

Magadh Sugar Financial Snapshot

| Particulars | FY20 | FY21 | FY22 | FY23 | FY24 |

| Sales Growth (%) | 23.9 | 3.9 | 4.5 | -4.2 | 15.0 |

| Net Margin (%) | 9.1 | 2.8 | 4.6 | 5.3 | 10.6 |

| RoE (%) | 15.5 | 4.9 | 7.7 | 7.9 | 15.6 |

| RoCE (%) | 23.7 | 15.2 | 14.4 | 14.1 | 23.1 |

Source: Equitymaster

In 9MFY25, total income increased by 20% to Rs 9.7 bn, driven by a 20% increase in sugar sales volume and higher realisation.

However, the margin declined from 16.5% last year to 10%, driven by higher production costs. With a lower margin, Magadh Sugar’s net profit fell 45% to Rs 0.38 bn.

Magadh Sugar and Energy Share Price Performance – 1 Year

Looking ahead, the Company aims to expand capacity across the sugar and distillery segments and enhance cogeneration capacity.

It has increased the crushing capacity of the Narakiagunj unit from 7,500 TCD to 10,000 TCD. It has also begun to convert the Siddhiwala distillery into a multi-feed distillery unit, which is expected to be operational by March 2025.

In addition, a new 100 KLPD multi-feed distillery and steam-saving measures for the Hasanpur unit have been planned.

It also sees growing demand for organic sugar, both domestically and internationally, as a potential opportunity to tap into premium markets.

#5 Triveni Engineering

Next on the list is Triveni Engineering.

Triveni Engineering is a diversified industrial group with leading market positions in the sugar and alcohol sectors. It is among India’s top 3 sugar manufacturers, with a sugar capacity of 70,500 TCD.

In addition, it is one of the largest companies producing bioethanol from sugarcane and grain-based feedstock. Its distillery capacity is 860 KLPD, and its cogeneration capacity is 104.5 MW, providing a well-diversified revenue base.

It is one of the leading market players in the engineered-to-order turbo gearbox industry through its power transmission segment. The company also operates in water and wastewater treatment businesses.

As of the third quarter of FY25, Triven’s revenue mix has shifted. The sugar business now accounts for 55% of the gross revenue, compared to 80% historically. The distillery accounts for 35%, and the balance comes from water and power.

Triveni Engineering Financial Snapshot

| Particulars | FY20 | FY21 | FY22 | FY23 | FY24 |

| Sales Growth (%) | 40.8 | 4.7 | -16.3 | 26.6 | -12.9 |

| Net Margin (%) | 7.6 | 6.3 | 10.9 | 36.4 | 9.2 |

| RoE (%) | 25.0 | 18.9 | 22.2 | 67.2 | 13.6 |

| RoCE (%) | 29.5 | 27.4 | 28.1 | 70.0 | 18.6 |

Source: Equitymaster

Over FY20-24, the company’s revenue grew at a CAGR of 6.4% to Rs 42.8 bn, and net profit grew at a 13% CAGR to Rs 3.9 bn. Return ratios remained strong, with RoE and RoCE averaging 29% and 35%, respectively.

In the first half of FY25, net revenue rose 7% to Rs 27.9 billion, driven by the distillery business and an increase in realisation. However, the margin narrowed to 3.3%, from 7.2% last year, leading to a net profit fall of 91%.

Triveni Engineering Share Price Performance – 1 Year

Further, the profitability of Triveni is expected to improve, aided by high sugar attainment and increased quantity from distillery operations. It is also increasing its production capacity for Indian -made Indian liquor business.

Its engineering division has an order backlog of 3.8 bn and Rs 19.8 bn in electricity and water business, which provides moderate -term revenue visibility.

It is also looking to expand its distillery and power transmission capacities to increase non-sugar revenue. To this end, it has committed Rs 0.6 bn in capex to expand the capacity of the power transmission business.

Conclusion

The sugar sector inherently remains a cyclical industry, impacted by strict government regulations like sugar price, MSP, and export controls. They continue to weigh on companies operating in the sector.

However, many players have been diversifying their revenue streams to reduce reliance on the cyclical sugar business. In this context, ethanal and power segments have emerged as key diversifiers.

That said, stock prices have already fallen up to 50% from their 52-week highs. Recovery hinges on easing export controls, policy clarity, ethanol blending targets, pricing, etc.

To make informed decisions, it’s crucial to assess a company’s fundamentals, corporate governance, and long-term prospects, rather than relying solely on market sentiment.

Happy investing.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such. Learn more about our recommendation services here…

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.